Filing...

Read More

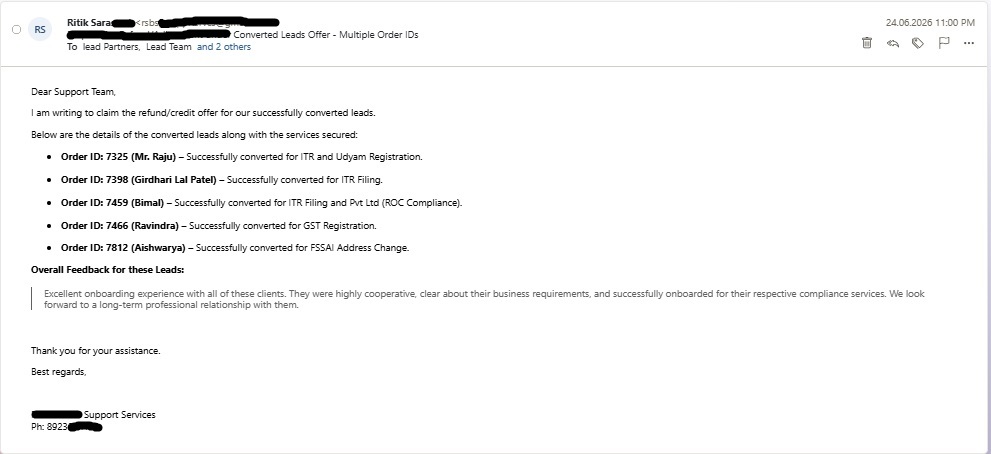

Excellent onboarding experience with all of these clients. They were highly cooperative, clear about their business requirements, and successfully onboarded for their respective compliance services. We look forward to a long-term professional relationship with them.

We registered our Private Limited Company through Digihunter. The entire process was transparent, quick, and professionally handled. Highly recommended.

“Digihunter helped us connect with GST clients consistently. The structured dashboard makes lead management easy.”

I was looking for an experienced tax consultant for my ITR filing. Digihunter connected me with the right professional, and the filing was completed smoothly

“We were able to onboard new ITR clients during peak season through Digihunter.”

As an NRI, I was confused about my Indian tax obligations. Digihunter connected me with a knowledgeable tax expert who handled everything professionally.

“The platform dashboard makes tracking leads simple. It saves time and improves follow-up efficiency.”

“During the financial year-end rush, Digihunter helped us onboard multiple ITR filing clients.”

Our GST Registration and monthly return filing are now completely hassle-free. The assigned professional explained everything clearly.

“Digihunter is a good platform for business service providers looking to expand their client base.”

The trademark registration process was completed faster than expected. The team kept us informed throughout the application.

Digihunter has helped us connect with genuine clients for Income Tax Filing and GST Registration. Their support team is responsive, and the lead management process is simple and efficient."